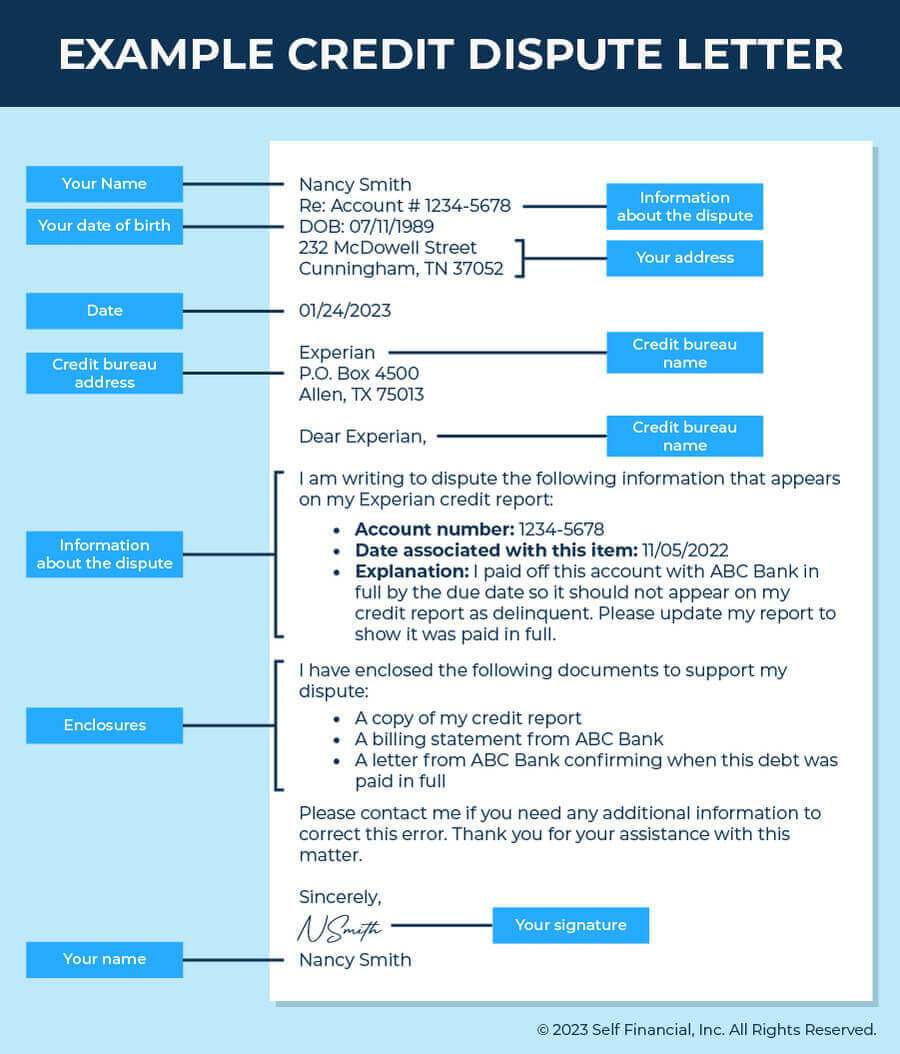

This new Law Performing

Military experts and you will activy obligation armed forces users can get Va financing with no money down for homes surpassing new conforming financing limit:

The newest laws plus apply at refinances. Evan Banning, president out-of Ca Housing and you will Lending, a bona fide-house broker and you will financial firm in the Hillcrest, told you he refinanced financing to possess a veterinarian and you will energetic reservist within the mid-January. The client had bought a home to own $1.eight million a couple of years prior to which have 10% down, however, failed to play with a Virtual assistant financing. Within the past Virtual assistant laws, refinancing will have needed their client to boost their family security. As an alternative, Mr. Forbidding offered an excellent re-finance of $1.62 billion no more funds off. He paid off the pace out of 4.125% to three.25%, the guy told you.

Laws Prior to 2020

Before the latest rules came into being, if you purchase property cherished over the local compliant home loan limitation you will must safety the new down-payment on part of the mortgage which is above the local restrict. Eg, for individuals who lived in a county in which the limit compliant mortgage limitation is actually $636,150 and you will desired to buy a house and therefore be more expensive than just so it, then you will have to generate a down payment away from twenty five% of the number outside the maximum. If you decided to purchase a home to have $836,150 having a good Virtual assistant financing you then will have to safety 25% of the loan amount above the regional limit.

- $836,150 – $636,150 = $two hundred,one hundred thousand

- $2 hundred,000 / cuatro = $50,100

When Is the greatest For you personally to Get A beneficial Virtual assistant Mortgage?

![]()

When you shop available for home financing, most people question if there’s a great “blast” to make use of. For the majority mortgage activities, there is no doubt you to trick field conditions connect with how much cash they are going to shell out. Although not, there’s no old advice about when you should – or ought not to – sign up for a beneficial Virtual assistant mortgage. The things which change the interest rates that will be linked to an average Va mortgage are varied and you will advanced you to definitely there is no hard-and-fast signal to mention in order to.

If you are considering a good Va financial, contact loads of qualified loan providers and get her or him precisely what the newest price are. Shoot for a be for whether prices provides recently crept right up or come down, and you may act properly. In any event, you will end up using not nearly as expensive people that do not be eligible for Va fund are likely to. As well as, without the care and attention of private home loan insurance rates and you will without the need to build a downpayment, you’ll be before the games economically anyway. Actually, the everyday criteria for Virtual assistant home loans can make anytime an excellent good-time to acquire that. This new Va loan work for is flexible and you may commonly used over the country. Here are use stats to possess fiscal 12 months 2018.

The new Downsides Off Virtual assistant Lenders

Would certainly be loan places Trail Side hard pressed discover a whole lot of drawbacks so you’re able to an effective Va home loan. Incase your qualify – we.elizabeth., you are a dynamic member of the us army, or a veteran – then you’ll definitely easily notice that advantages of such an effective mortgage much exceed the few cons. However, to produce a knowledgeable and most educated choice you are able to, you need to realize about the latest drawbacks and you may disadvantages regarding Va loans. Knowing just what you’re getting your self on is definitely a idea. Generally, area of the downsides regarding a great Virtual assistant mortgage was:

Even though they are very different based where you live in the united states, you can find limits about how precisely high of a great Va financial you could remove. Those who are looking to buy an incredibly expensive household, for-instance, can be disappointed by the financing restrictions that are imposed from the the fresh Virtual assistant home loan program. If your family that you like to invest in exceeds the borrowed funds constraints set by Virtual assistant home loan system, you are going to need to finance the bill thanks to another home loan system. This can surely negate the benefits of with the Virtual assistant domestic loan system. Still, new restriction in most portion is $729,000; with the vast majority men and women, you to definitely number is over adequate for just what he’s looking on.